Housing market shows resilience, office segment on strong footing

Annual residential sales have exceeded the launches for the first time post 2016; Office segment achieved a milestone with over 46 mn sq ft of net absorption

- Mumbai and Bengaluru continued to dominate new launches, taking more than 60% of the overall launches during the year

- Except for Mumbai, all the other cities witnessed a dip in new launches in 2019 when compared to 2018; Kolkata saw the maximum drop of 62% y-o-y in new launches

- Unit absorption in Mumbai and Delhi NCR has helped in the spike in overall sales

- A sizeable 55% of new supply was in the affordable and mid-price segment; supply mainly concentrated in the peripheral areas of the cities

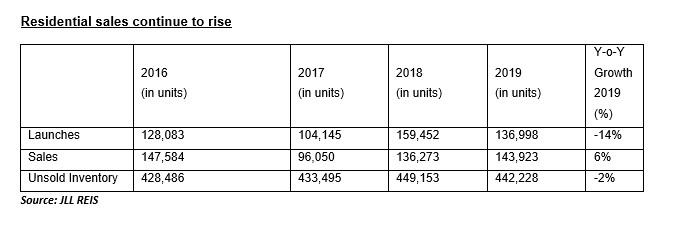

Annual sales have exceeded the annual launches for the first time since 2016, indicating further stability in the residential market, according to the latest JLL Report, India Market Update 2019, released today.

Witnessing a drop of 14% in unit launches, the year 2019 saw a substantial decrease to 136,998 when compared to 159,452 units launched in 2018. On the sales front, the year saw an increase of 6% with 143,923 units sold in 2019 as compared to 136,273 units in 2018.

The report added, a weak last quarter that witnessed new launches of 26,405 units, a decrease of 31% when compared to Q4 2018, contributed majorly to the decline in new launches. Mumbai remained the only city in the country to witness that saw a hike in launches. All other cities witnessed a drop in launches in 2019 in comparison to 2018.

The affordable and mid-income housing segments (ticket size of up to INR 10 million in Mumbai and INR 7.5 million across other cities) still form the majority of the launches and supply. However, the collective share of the two segments has also dropped to 55% in 2019 as compared to 66% in 2018, the report added. Pune tops the list, with 84% of the new supply falling in the affordable and mid-income category.

The launches in these segments were mostly concentrated in the peripheral areas of the cities, which have the availability of larger land parcels at comparatively lower costs. The drop can be attributed to the fact that there is already an existing substantial number of under-construction units in these segments. Interestingly, larger markets such as Mumbai, Bengaluru and Delhi NCR witnessed more launches in these ticket-sizes as compared to markets like Hyderabad and Kolkata.

On the sales front, the report added, while the first half of 2019 witnessed a substantial jump in sales of 22% on a y-o-y basis, the second half of the year recorded a 9% dip in the offtake of units. The prolonged economic slowdown led by weak consumer demand has been manifesting itself in the form of sluggish sales with buyers postponing their purchase decisions.

While the three key markets of Mumbai, Bengaluru and Delhi NCR continued to account for a major chunk of the total sales, the number of sold units in Hyderabad increased by 21% y-o-y in 2019. In the last quarter (October to December) of 2019, Mumbai has so far defied market trends and has been the only city to register a sales growth when compared to Q4 2018.

Ramesh Nair, CEO & Country Head – India, JLL, said, “The residential market has seen a gradual shift in consumer behaviour. Homebuyers are now looking at mostly ready-to-move-in apartments or under-construction properties by developers who have good track records pertaining to completion of projects. Recent reforms and developers’ focus on the delivery of projects will lead to more supply in 2020 and the revival of buyers’ sentiments. We believe sales will continue to rise in future and are likely to increase beyond the pre-demonetization year of 2016. The revival signs of the residential segment will be more visible through affordable housing demand which will drive long term institutional funds to invest in this segment.”

The surge in sales will primarily hinge on enhanced consumer confidence, which in turn depends upon the effective implementation of progressive government policies and economic growth registering a comeback.

The report added, with sales surpassing new launches, there has been a decline of 2% in unsold inventory. Samantak Das, Chief Economist and Head of Research & REIS, JLL India, said, “All cities except for Mumbai and Bengaluru witnessed a decline in inventory levels. An assessment of years to sell (YTS) reveals that the YTS across the seven cities declined from 3.9 years in 2018 to 3.2 years by the end of 2019 which signals a better level of inventory management.”

The report added, residential price increase has remained range bound (below up to 4%) in most of the cities. On the back of a surge in demand, Hyderabad has been the only exception, recording a 9% y-o-y increase in price. “Developers are keen to get the sales volume back in the market rather than hiking the price,” added Das

A bullish office market

India office market has set a new benchmark and recorded a historic high, both in net absorption and new completions. While 46.5 mn sq ft of space got absorbed nearly 52-mn sq ft of Grade A office space was completed in 2019, according to the report. The trend is phenomenal as the last such spike in net absorption was witnessed in the year 2011. The market reported a net absorption of 37 mn sq ft in 2011.

Over 46 mn sq ft in 2019 as compared to over 33 mn sq ft in 2018, the year witnessed a jump of 40% in net absorption. The strong expansion of IT/ITeS (42% of overall leasing) and co-working operators (14% of overall leasing) in cities with strong fundamentals and planned infrastructure improvements has led the strong growth in demand so far, the report added. The current pace of absorption is expected to continue in 2020 as well and is likely to cross the 40 mn sq ft mark.

Bengaluru, Delhi NCR and Hyderabad accounted for nearly 70% of the net absorption in 2019. As against this, Mumbai witnessed a marginal drop of 2% y-o-y in net absorption on the back of limited relevant supply despite strong latent demand from large occupiers, the report added. Competing with bigger markets, Hyderabad recorded a net absorption of 10.5 mn sq ft in 2019.

With the net absorption of more than 5 mn sq ft in the last quarter (October-December), the Delhi-NCR market too achieved a new yardstick of around 11 mn sq ft in 2019.

The country also witnessed stronger new completion during the year 2019. Registering a growth of 45%, y-o-y, 51.6 mn sq ft of new office space was added to the stock in 2019. In line with net absorption, Bengaluru, Delhi NCR and Hyderabad together accounted for nearly 80% of the new completions in 2019. Each of these three cities witnessed more than 13 mn sq ft of new completions, with Bengaluru leading the pack at 13.9 mn sq ft.

“Establishment of REIT will lead to developers thinking more long-term and building better quality assets. With almost all top 10 office developers having institutional partners, we expect a further flight to quality, enhanced technical upgrades of existing portfolio, smart buildings, more focus on wellness and human experience. Future demand is expected to come from the datacentre industry as well. Occupiers will continue their focus on cost, talent, agility, compliance and productivity,” added Nair.

The momentum in new completions is expected to continue in 2020, hovering at the 50-mn sq ft mark. Hyderabad will continue its rise in the office market with more than 13 mn sq ft of office space expected to be completed in the next year.

“Investment sentiments in office space have remained strong in the country leading to a general drop in vacancy levels from the previous year. Cities like Bengaluru (5.3%), Hyderabad (7.2%), Chennai (8.7%) and Pune (5.3%) continued to hover at single-digit vacancies on the back of sturdy demand for Grade A offices. The increased demand in these markets manifests themselves in the form of rentals growing between 4%-8% on a Y-o-Y basis. In bigger cities like Mumbai and Delhi-NCR, the prime business districts have recorded low single-digit vacancy,” added Das.

About JLL

JLL (NYSE: JLL) is a leading professional services firm that specializes in real estate and investment management. JLL shapes the future of real estate for a better world by using the most advanced technology to create rewarding opportunities, amazing spaces and sustainable real estate solutions for our clients, our people and our communities. JLL is a Fortune 500 company with annual revenue of $18.0 billion, operations in over 80 countries and a global workforce of more than 93,000 as of December 31, 2019. JLL is the brand name, and a registered trademark, of Jones Lang LaSalle Incorporated. For further information, visit jll.com.